Living in California offers many advantages: great weather, vibrant cities, and strong job opportunities. However, it also comes with unique challenges, from devastating wildfires and earthquakes to everyday risks like theft and water damage. If you rent your home, protecting yourself financially is essential.

Renters insurance in California helps cover your personal belongings, protects you if someone gets hurt in your apartment, and can even help pay for temporary housing if your rental becomes unlivable. Despite these benefits, many renters still lack coverage.

This complete guide will help you understand why coverage matters and how to protect yourself in one of the nation's highest-risk states.

California's renter landscape

California has one of the largest renter populations in the country and one of the highest risk profiles for natural disasters.

Renters vs. homeowners: California vs. United States

- California: Roughly 44% of households are renters.

- United States: About 35% of households rent their homes.

California’s high housing costs, compared to other states, mean more people rent for longer periods and invest more heavily in their belongings. That means there’s even more need for protection.

Share of active renters insurance policies: California vs. United States

Even though renters insurance is affordable, coverage rates remain surprisingly low:

- California: Nearly one in two (49%) California rental households are protected, leaving millions of renters uninsured.

- United States: About 48% of renters have renters insurance.

This gap means many renters would have to pay out of pocket after a loss.

Average renters insurance cost: California vs. United States

Renters insurance is one of the most affordable types of insurance available, and renters in the Golden State pay, on average, slightly less than the national average.

- California average: $19 per month

- National average: $23 per month

Several factors may cause renters insurance prices to fluctuate, including:

- Environmental risks

- Location and ZIP code

- Building type and property requirements

- Coverage limits and deductible selected

- The insurance company or underwriter pricing the policy

For example, renters in higher wildfire-risk areas of California may see higher premiums than renters in lower-risk neighborhoods. Similarly, newer buildings with updated safety features may qualify for lower rates.

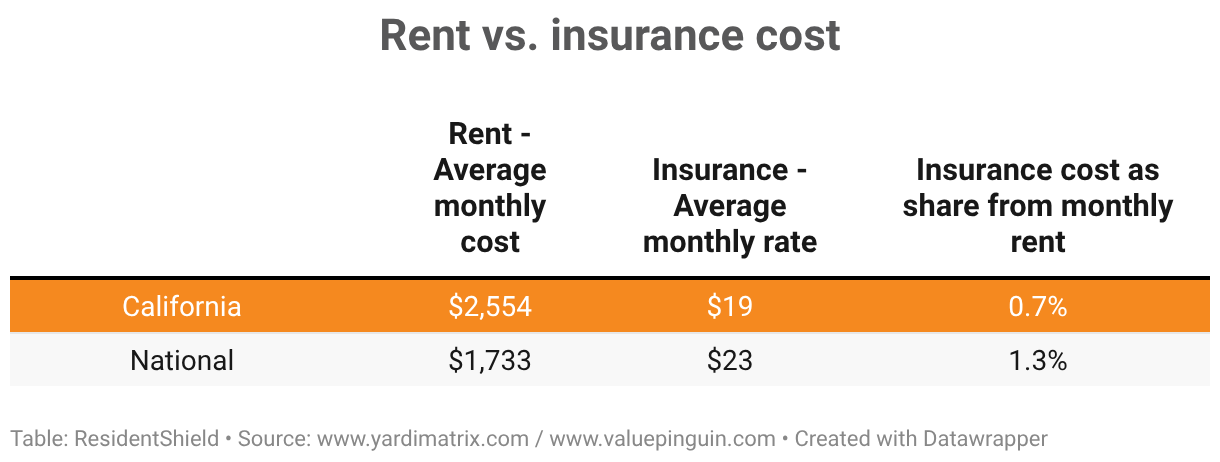

Comparing insurance costs to rent: California vs. United States

Renters insurance remains one of the few housing-related costs that stays low, even in expensive rental markets. Comparing rent prices with renters insurance premiums at both the national level and in California shows just how small the cost of coverage really is.

California:

- Average monthly rent: ~$2,554

- Average monthly renters insurance cost: ~$19

- Insurance cost as percentage of rent: Well under 1%

United States:

- Average monthly rent: ~$1,733

- Average monthly renters insurance cost: ~$23

- Insurance cost as percentage of rent: Less than 2%

Despite California's higher rent costs, renters actually pay less for insurance than the national average, making coverage an exceptional value.

How much coverage do renters choose?

Coverage needs vary, but the patterns are clear. Across the United States, most renters choose personal property coverage between $20,000 and $24,999. In California, most renters opt for coverage between $15,000 and $19,999.

The most common coverage ranges in California, accounting for over 70% of all renters insurance policies, are:

- $15,000–$19,999

- $20,000–$24,999

- $10,000–$14,999

- $25,000–$29,999

- $30,000–$34,999

This shows that most California renters insure between $10,000 and $35,000 worth of personal belongings.

Is renters insurance mandatory in California?

No, renters insurance is not legally required by federal or California state law.

However, many landlords require renters insurance as part of the lease agreement. Even when it’s not required, skipping coverage puts you at significant financial risk when:

- Your landlord’s insurance doesn’t cover your belongings.

- You could be personally responsible if someone gets hurt in your rental.

- You may need to pay out of pocket for temporary housing after a covered loss.

What does renters insurance cover in California?

A standard renters insurance (HO4) policy in the Golden State includes three main types of coverage: personal property, liability, and loss of use.

1. Personal property coverage

This protects your belongings if they’re damaged or stolen due to covered events like:

- Fire or smoke

- Theft or vandalism

- Water damage from burst pipes

- Windstorms

Covered items typically include furniture, clothes, electronics, and kitchenware.

2. Liability coverage

If someone gets injured in your rental or you accidentally damage someone else’s property, liability coverage helps pay for:

- Medical bills

- Legal fees

- Settlements or judgments

3. Loss of use (Additional Living Expenses)

If your rental becomes unlivable due to a covered event, this coverage helps pay for:

- Hotel stays

- Temporary rentals

- Meals and extra living costs

What are the most common risks in California?

California ranks first out of 56 U.S. states and territories on the FEMA National Risk Index. That makes it the highest-risk state in the country based on expected annual losses from natural hazards.

For renters, this means a higher likelihood of property damage, temporary displacement, and unexpected expenses.

Top risk factors in California

Based on FEMA's Expected Annual Loss Scores (scale of 0–100), California's highest risk factors include:

- Wildfire: 100

- Earthquake: 100

- Drought: 100

- Inland flooding: 100

- Landslides: 98

How these risks affect renters insurance claims

If you did opt for renters insurance, here’s how your plan would or wouldn’t cover you during natural disasters:

- Wildfire coverage: Fire and smoke damage, including damage from wildfires, is generally covered under standard renters insurance policies in California.

- Earthquake coverage: Standard renters insurance typically doesn't cover earthquake damage to your belongings. You usually need to purchase additional earthquake coverage as an add-on or separate policy. Providers like ResidentShield Insurance include optional earthquake coverage in California.

Choosing the right renters insurance

When selecting renters insurance in California, look for providers that offer:

- Simple online enrollment

- Coverage that meets lease requirements with instant proof of insurance

- Affordable plans designed specifically for renters

- Easy policy management tools

- Strong reputation with property managers

Companies like ResidentShield specialize in modern renter needs, offering streamlined processes and coverage options tailored to today's rental market.

Renters insurance in California is one of the easiest and most affordable ways to protect yourself, your belongings, and your financial future. While it’s not required by law, it’s a smart decision in a state with high housing costs and elevated natural risks.

With costs below the national average and coverage that protects what matters most, renters insurance turns uncertainty into confidence.

Key takeaways:

- California has a higher renter population than the national average, with nearly half lacking renters insurance.

- While not legally required, renters insurance is often required by landlords.

- The average policy cost is minimal compared to monthly rent expenses.

- California's high-risk environment makes coverage especially valuable.

Frequently asked questions

A: If your apartment’s walls crack, your floor shifts, or your building suffers structural damage, your renters insurance likely won’t step in. However, landlord's insurance policy typically covers the physical structure of the building.

To protect your valuables against earthquake damage, you usually need an add-on or a separate earthquake insurance policy. ResidentShield Insurance includes optional earthquake coverage in California.

A: Yes. Fire and smoke damage, including damage caused by wildfires, is generally covered under renters insurance in California.

A: The right amount depends on the value of your belongings. Most California renters choose between $15,000 and $25,000 in personal property coverage. To determine your needs, create an inventory of your belongings and estimate their replacement costs.

Methodology

This article's data was compiled by our analytics team using publicly available housing statistics, insurance industry reporting, aggregated market averages from recent years, and market intelligence provided by our sister company, Yardi Matrix. Cost estimates reflect statewide averages and may vary by city, building type, and coverage limits.

All figures are intended for educational purposes and should be used as general guidance when evaluating renters insurance in California.

Sources

- The Insurance Information Institute. Average Homeowners Losses, 2019-2023. https://www.iii.org/table-archive/20887, accessed on January 29, 2026.

- National Association of Insurance Commissioners (May 2025). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2022. https://content.naic.org/sites/default/files/publication-hmr-zu-homeowners-report.pdf, accessed on January 29, 2026.

- Lindsay Bishop (Dec 2025). Average Cost of Renters Insurance (2026). https://www.valuepenguin.com/average-cost-renters-insurance, accessed on January 29, 2026.

- US Census Bureau. American Housing Survey (AHS). https://www.census.gov/programs-surveys/ahs/data/interactive/ahstablecreator.html, accessed on January 29, 2026.

- The Federal Emergency Management Agency (FEMA). National Risk Index Data (Dec 2025). https://www.fema.gov/about/openfema/data-sets/national-risk-index-data, accessed on January 26, 2026.